Financial planning

1. Raising finance: Start-up capital

Before you start your business you will need a sum of money to set things up. This money is called start-up capital.

Start-up capital is used to purchase fixed assets (called capital expenditure). Working capital is also needed. This is used to fund the trading activity of the business eg buying materials and/or stocks (called revenue expenditure).

How do businesses raise this initial start-up capital?

There are several possible sources, but we will focus on four:

Chapter 8 - Raising finance

2. Costs, revenues & profit

When businesses spend money it is called a cost. When business receive money from selling products it is called revenue.

Profit = total revenue - total costs.

Task 2 - Costs, revenues & profit Answer using the link below

Chapter 11 - Calculating costs, revenues & profits

Costs for trading at NIS

3. Calculating the break-even point

It is important for you to know how many products your business must sell in order to pay off the fixed costs and start making profits. This can be achieved through a break-even chart, or by calculation.

Chapter 12 - Break-even analysis

Break-even is the quantity of product sold where total revenue = total cost, ie where zero profit is made.

Contribution = price - unit variable cost. It is money that comes from selling products that goes towards paying the fixed costs. Once the fixed costs are covered further contribution becomes profit.

Before you start your business you will need a sum of money to set things up. This money is called start-up capital.

Start-up capital is used to purchase fixed assets (called capital expenditure). Working capital is also needed. This is used to fund the trading activity of the business eg buying materials and/or stocks (called revenue expenditure).

How do businesses raise this initial start-up capital?

There are several possible sources, but we will focus on four:

- issuing shares (for limited companies only)

- bank loans

- venture capital/business angels

- personal sources.

Chapter 8 - Raising finance

2. Costs, revenues & profit

When businesses spend money it is called a cost. When business receive money from selling products it is called revenue.

Profit = total revenue - total costs.

Task 2 - Costs, revenues & profit Answer using the link below

Chapter 11 - Calculating costs, revenues & profits

Costs for trading at NIS

3. Calculating the break-even point

It is important for you to know how many products your business must sell in order to pay off the fixed costs and start making profits. This can be achieved through a break-even chart, or by calculation.

Chapter 12 - Break-even analysis

Break-even is the quantity of product sold where total revenue = total cost, ie where zero profit is made.

Contribution = price - unit variable cost. It is money that comes from selling products that goes towards paying the fixed costs. Once the fixed costs are covered further contribution becomes profit.

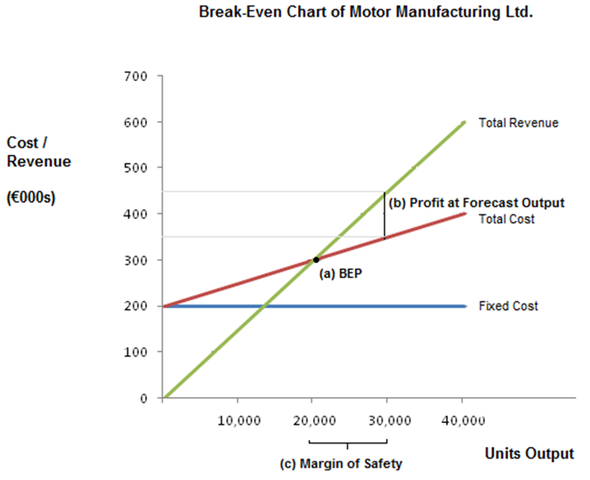

An example of a break-even chart

Break-even can be found in two ways:

a) By calculation

BEP = Total fixed costs / contribution per unit

b) By chart

a) By calculation

BEP = Total fixed costs / contribution per unit

b) By chart

4. Preparing cash flow forecasts

A cash flow forecast is a plan of how cash will flow into and out of the business over a period of time in the future.

Cash flow forecast Keynote

Chapter 13 - Cash flow forecasts

Cash flow example

Task 4 - Prepare a cash flow forecast for your business

A cash flow forecast is a plan of how cash will flow into and out of the business over a period of time in the future.

Cash flow forecast Keynote

Chapter 13 - Cash flow forecasts

Cash flow example

Task 4 - Prepare a cash flow forecast for your business